By Jesse Sommer, John West and Rick Hartmann III, Guy Carpenter

Once deemed a market of last resort, legacy insurers have seen a rise in transactions centered on the transfer of aged liabilities. These “legacy” transactions are now an integral part of a captive insurer’s capital management strategy.

Why are captive insurers suddenly very focused on proactively managing their legacy reserves?

A confluence of macroeconomic factors including economic inflation, social inflation, and volatility in the equity markets is creating uncertainty around embedded return assumptions and pressuring reserve adequacies of captive insurers. As a result, captive managers are seeking retroactive or legacy reinsurance solutions that will manage volatility and protect the balance sheet from adverse development or reserve deterioration.

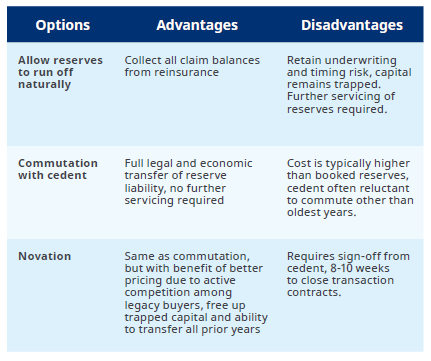

What options do captive insurers and risk managers have at their disposal?

Captive managers have essentially 3 options when it comes to a captive’s legacy reserves:

Why captive insurers should be considering a novation?

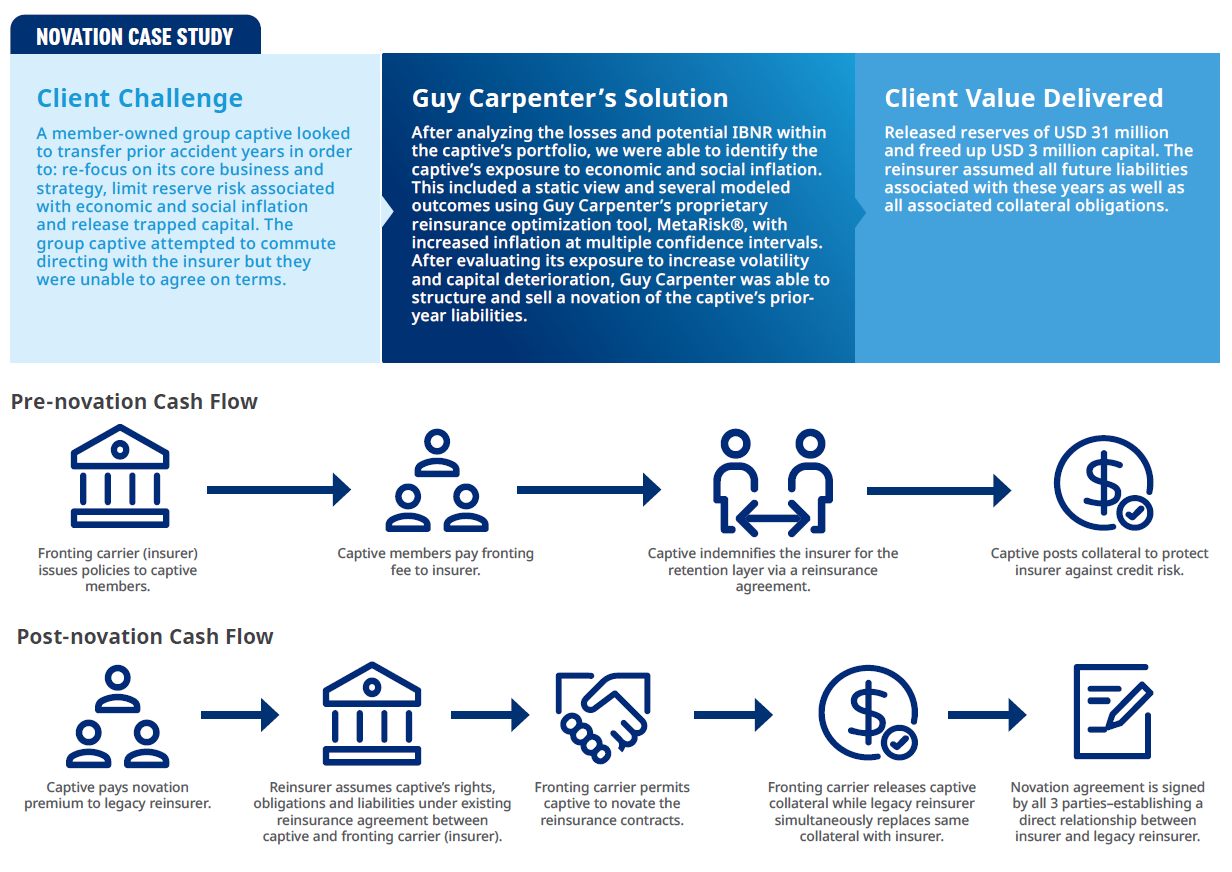

In addition to bringing price certainty to the captive’s reserves, cleaning up the balance sheet, and allowing captives to refocus on core business–competition among legacy writers ensures the most advantageous terms for the captive. Acquirers of legacy liabilities are often backed by sophisticated and sizable hedge funds whose investment expertise translates into better pricing terms for the captive. The current high-yield environment is especially appealing to these investors. Other factors, such as the ability to diversify their books and leverage their off-shore status, leave them well-positioned to offer more aggressive discounting of reserves.

Execution and Timing

While a non-binding indication or bid could be offered within 2 to 3 weeks, a typical novation transaction needs 10-12 weeks of lead time for execution. This includes data gathering, modeling, marketing the placement, receipt of a non-binding indication and finalizing the placement. Generally, the following data is needed to structure a novation solution:

- Recent actuarial report

- Recent loss run

- Program parameters (e.g., years to be novated, lines of business, policy limits)

- Current collateral requirement

Captive insurers and risk managers don’t need to wait until their captives have experienced reserve deterioration or adverse development before considering a novation. By proactively managing reserves, captive insurers can execute a novation as a hedge against adverse development or reserve deterioration. They can allocate capital to take advantage of current market conditions in lieu of continued exposure to the uncertainties and burdens associated with expired policy years.

Putting the Past Behind You-A Seller's Guide to Novations

Once deemed a market of last resort, legacy insurers have seen a rise in transactions centered on the transfer of aged liabilities. These “legacy” transactions are now an integral part of a captive insurer’s capital management strategy.